You can always continue to grow your savings for your retirement, it doesn’t matter if you are just starting out or you have 6 months left before you plan to retire. You can always add to your nest egg. When planning for retirement, the truth is that the earlier you start saving and investing, the better off you’ll be, thanks to the power of compound interest. Even if you began saving late or have yet to begin, it’s important to know that you are not alone, and there are steps you can take to increase your retirement savings.

It’s never too early or too late to plan for and achieve your retirement goals. Even if you are living paycheck to paycheck, start small by contributing 1% of your paycheck to the 401(k) and then increasing the contribution 1% each year moving forward. It may seem like a small amount, but it is a start and over time it will add up. A 1% contribution will likely have little impact in your take-home pay as the contribution to your 401 (k) is pre-tax. If your company matches 3% then you should contribute the 3% to start, if at all possible, to maximize the matching and then increase it by 1% each year after.

One of the reasons it’s important to start saving early if you can is that yearly contributions to IRAs and 401(k) plans are limited. The good news? Once you reach age 50, you’re eligible to go beyond the normal limits with catch-up contributions to IRAs and 401(k)s. So if over the years, you haven’t been able to save as much as you would have liked, catch-up contributions can help boost your retirement savings.

Consider establishing an individual retirement account (IRA) to help build your nest egg. You have two options: Learn whether a Traditional IRA may be right for you depending on your income and whether you and/or your spouse have a workplace retirement plan. Contributions to a Traditional IRA may be tax-deductible (see advise from your retirement advisor or accountant on this) and the investment earnings have the opportunity to grow tax-deferred until you make withdrawals during retirement. Another option is a Roth. They are funded with after-tax contributions, so once you have turned age 59½, qualified withdrawals, including earnings, are federal-tax-free (and may be state-tax-free) if you’ve held the account for at least five years.

Automate your savings, pay yourself first! Make your retirement contributions automatic each month and you’ll have the opportunity to potentially grow your nest egg without having to think about it.

Don’t forget to set a goal for yourself. Knowing how much you’ll need not only makes the process of saving and investing easier but also can make it more rewarding. Set benchmarks along the way, and gain satisfaction as you pursue your retirement goal.

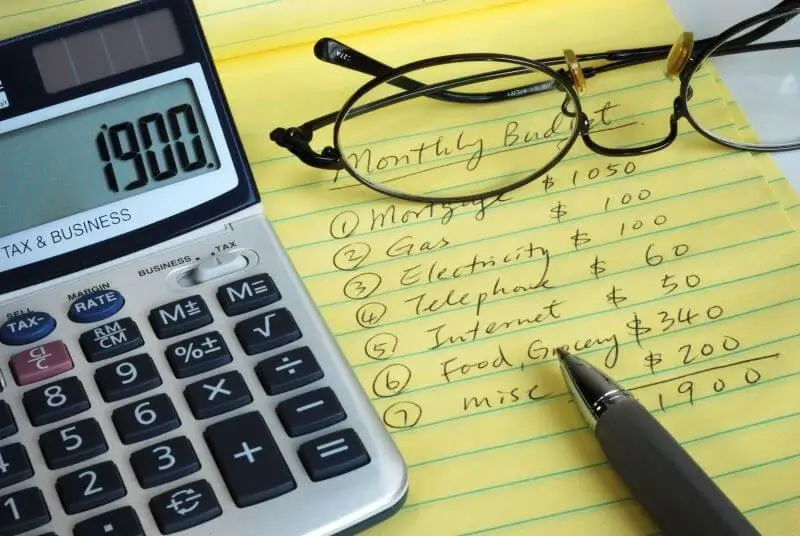

Examine your budget. Determine where your money is going and find places you can reduce spending, so you have more to save or invest. Every time you receive a raise, increase your contribution percentage. Dedicate at least half of the new money to your retirement plan.

Recognizing the need to put money away for retirement is the first step. Understand how much you want to sock away for retirement and find creative ways to increase your contributions.